{kind=link}

How Aerodrome Became Base’s Liquidity Engine: A Deep Dive

The first impression of Aerodrome on Base is almost deceptive: another ve(3,3)-style DEX on a new Layer 2, inheriting architecture from Velodrome on Optimism. Yet a closer look at on-chain metrics, protocol integrations, and governance incentives reveals something more foundational. Aerodrome has effectively become the liquidity coordination layer for Base, shaping where capital flows, which tokens thrive, and how the ecosystem prices risk.

This review examines how Aerodrome evolved into Base’s liquidity engine, using reported data from DeFiLlama, Dune Analytics, Nansen, and protocol documentation as of February 20, 2026. It follows an arc from “Velodrome clone” to “MetaDEX infrastructure,” evaluates its technical and economic design, and weighs the upside against its concentration and governance risks.

1. Executive Summary

Aerodrome Finance is now the dominant liquidity hub on the Base network, the Ethereum Layer 2 built with the Optimism OP Stack and incubated by Coinbase. According to dashboards cited from DeFiLlama and Dune Analytics, Aerodrome holds roughly $2.8 billion in total value locked (TVL) as of mid-February 2026, or about 62% of Base’s reported ecosystem TVL of $4.5 billion. That concentration alone signals its centrality to Base’s DeFi stack.

Over the 30-day period from January 21 to February 20, 2026, Aerodrome facilitated approximately $18.7 billion in trading volume and hosted around 1.2 million swaps, with an average of 45,000 transactions per day. Active user counts (unique addresses interacting with Aerodrome contracts) reached roughly 156,000 in the same window, with Slipstream concentrated-liquidity pools now making up about 35% of total liquidity.

At first glance, these are the numbers of a strong DEX. Combined with Aerodrome’s vote-escrow (veAERO) governance, bribe-driven emissions markets, and deep integration with Base-native protocols, they describe something closer to a liquidity engine. Protocols on Base do not just list tokens on Aerodrome; they increasingly coordinate emissions, bribes, and LP incentives through it.

The picture is not unambiguously bullish. The protocol’s reliance on emissions and bribes, concentration of veAERO voting power, and dependency on Base’s centralized sequencer and Coinbase’s regulatory posture all introduce meaningful risks. Yet, from a Base ecosystem standpoint, Aerodrome currently sits in a category of its own: it is the default pricing and liquidity venue for a majority of Base assets, and its design gives it strong path dependence.

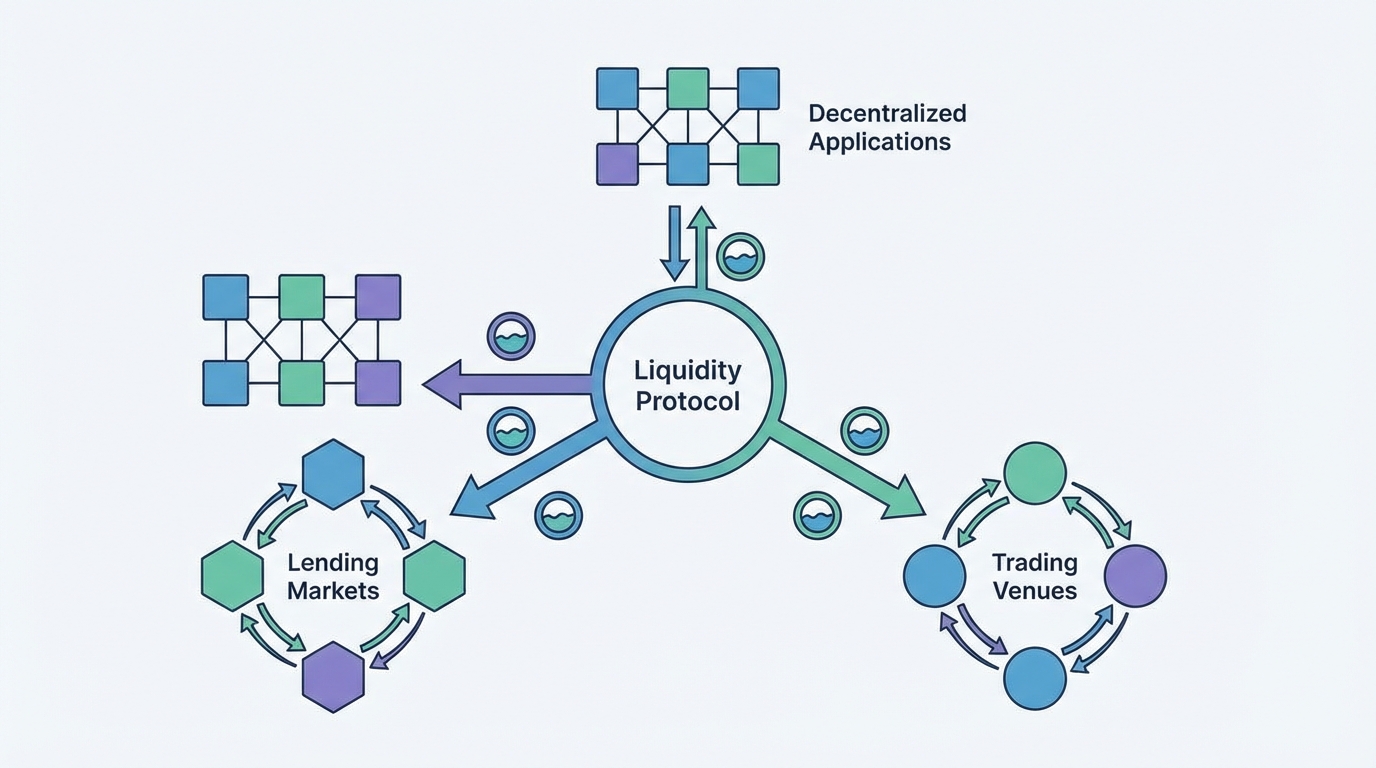

2. Protocol Overview

Aerodrome Finance is a decentralized exchange (DEX) deployed on Base and developed by the same team behind Velodrome on Optimism. Launched in August 2023, it was purpose-built to serve as Base’s core liquidity hub, plugging Velodrome V2’s MetaDEX architecture into a cheaper, higher-throughput environment backed by Coinbase’s distribution.

Conceptually, Aerodrome sits at the intersection of three major DeFi designs:

- Uniswap-style AMM routing with volatile and stable pools, plus Uniswap V3-like concentrated liquidity via Slipstream.

- Curve’s vote-escrow model – users lock the native AERO token to receive veAERO, a non-transferable voting power that decays over time.

- Convex-like incentive markets – protocols bribe veAERO holders to direct emissions to their liquidity pools, effectively renting governance power.

The native token AERO underpins this system. Users lock AERO into the VotingEscrow contract to receive veAERO, which grants:

- Voting power to direct weekly AERO emissions across liquidity gauges.

- Eligibility to earn 100% of protocol trading fees routed to voters.

- Bribes paid by external protocols that want veAERO attention on their pools.

As of February 20, 2026, the circulating AERO supply is reported at about 1.65 billion tokens, with roughly 28% locked as veAERO. Around 10% of veAERO is held by Base-native protocols, giving builders a direct lever over emissions and deepening the ecosystem feedback loop. Weekly emissions via the Minter contract, combined with fees and bribes, create a powerful incentive flywheel for liquidity formation.

Initially, this design could be dismissed as “just Velodrome on a new chain.” But as Base’s user base and TVL expanded in late 2024 and 2025, Aerodrome’s ve(3,3) model began to reshape how new tokens launch, how stablecoins maintain deep liquidity, and how Base-native projects compete for attention.

3. Technical Analysis

Architecture and Innovation

Aerodrome’s core architecture mirrors Velodrome V2 and blends AMM logic with governance-driven incentives. At its heart are several key contracts:

- Pool: manages token reserves and mints LP tokens.

- Minter: handles weekly AERO emissions and updates epochs.

- Voter: aggregates veAERO votes and allocates emissions across Gauges.

- Gauge: connects LP positions to emissions, collecting and distributing rewards.

- VotingEscrow: converts locked AERO into veAERO, with time-decaying voting power.

Liquidity is split into three main types:

- Volatile pools using a constant-product formula for uncorrelated asset pairs.

- Stable pools using a stableswap-like curve optimized for low-slippage, correlated assets (e.g., USDC–USDT).

- Slipstream pools, Aerodrome’s concentrated-liquidity implementation, where LPs supply capital within custom price ranges, greatly improving capital efficiency.

A Protocol Router sits atop these pools, routing trades across the optimal path and using 30-minute time-weighted average prices (TWAPs) to mitigate short-term price manipulation without relying heavily on external oracles. The design borrows Uniswap V3’s efficiency, Curve’s stableswap, and Convex’s governance markets, but packages them into a Base-native MetaDEX that is deeply entwined with the chain’s broader liquidity topology.

Smart Contract Design and Complexity

From a smart contract perspective, Aerodrome is neither minimalistic nor trivial. Token and reward flows can be summarized as:

- Voter::distribute triggers Minter::updatePeriod, which mints new AERO per epoch.

- Newly minted AERO is routed via the Voter to Gauge contracts for each pool.

- Fees accrue to FeesVotingReward, while bribes are handled by BribeVotingReward.

- Rebase-like rewards for managed positions are handled via LockedManagedReward.

This interconnected design is powerful but raises the bar for security. The team addressed this with multiple audits from firms such as PeckShield and Quantstamp in 2023, with reports indicating no unresolved critical vulnerabilities at launch. Continuous upgrades-particularly around Slipstream optimization and Flashblocks integration-mean the attack surface is not static, but the track record to date has been clean, with no major public exploits reported.

Scalability and Performance on Base

Base’s low fees and high throughput (compared to Ethereum mainnet) amplify Aerodrome’s design. Swap costs are typically below 0.05% including gas, which makes complex routing and governance interactions economically viable for smaller users. Planned integration with Flashblocks-an enhancement targeting sub-second effective block times—aims to further reduce latency and slippage, which is particularly attractive for market makers and higher-frequency trading strategies.

The adoption of concentrated-liquidity Slipstream pools marks a turning point in Aerodrome’s technical evolution. By February 2026, Slipstream pools account for an estimated 35% of TVL, significantly increasing capital efficiency and fee density. This shift moves Aerodrome closer to Uniswap V3’s performance profile while retaining the ve(3,3) incentive layer that Uniswap lacks.

Integration Capabilities and Developer Activity

Aerodrome’s open Voter and Gauge architecture makes it unusually integration-friendly. Any protocol on Base can deploy a pool, register a gauge, and then accumulate veAERO (or bribe veAERO holders) to attract emissions to its own liquidity. This has created a quasi-standard playbook for Base-native tokens: launch pool on Aerodrome, bootstrap via bribes, and then lock AERO in treasury to secure ongoing emissions.

Developer activity around Aerodrome backs this up. BaseScan data for late January to late February 2026 indicates roughly 47 new contracts deployed that interact with Aerodrome’s Voter and Gauge contracts, and around 112 unique addresses deploying integrations in Q1 2026. GitHub activity shows roughly 240 commits in the prior 30 days, focused heavily on Slipstream and infrastructure optimizations. Around 65 new pools have reportedly been created using Aerodrome SDKs, and roughly 30 forks of its gauge contracts have been used for custom reward mechanisms.

This level of activity signals that builders increasingly treat Aerodrome as the default liquidity backend for Base, rather than just another DEX competitor.

4. Market Analysis

Current Adoption Metrics and Growth Trajectory

According to DeFiLlama and Dune dashboards as of February 20, 2026, Aerodrome has:

- ~$2.8 billion TVL, or ~62% of Base’s reported total TVL.

- ~$18.7 billion in 30-day trading volume (Jan 21–Feb 20, 2026).

- ~1.2 million swaps in that period, averaging ~45,000 transactions per day.

- ~156,000 active user addresses over the same 30-day window.

Volume grew roughly 25% month over month into February 2026, driven in large part by the growth of Slipstream pools and increasing institutional-style market making. A temporary 12% dip in daily active users in early February suggests sensitivity to broader market conditions, but TVL remained stable, indicating that deeper liquidity providers are stickier than purely speculative retail flows.

Competitive Landscape on Base and Beyond

On Base itself, Aerodrome holds a decisive lead in both TVL and DEX volume. Estimated Base DEX market shares (February 2026) look approximately as follows:

- Aerodrome: ~62% of Base TVL (~$2.8B), ~$18.7B 30-day volume.

- Uniswap V3: ~18% TVL (~$0.8B), ~$4.2B 30-day volume.

- PancakeSwap: ~8% TVL (~$0.36B), ~$1.9B 30-day volume.

- Baseswap and other forks: low- to mid-single-digit shares.

In terms of positioning, Aerodrome sits somewhere between Uniswap V3 and Curve/Convex:

- Like Uniswap V3, it offers concentrated liquidity and efficient routing.

- Like Curve, it focuses heavily on stable and correlated asset pairs with vote-escrowed governance.

- Like Convex, it externalizes governance markets via bribes and gauges.

Compared to Velodrome on Optimism, Aerodrome reportedly holds about 3x more TVL, bolstered by Base’s lower fees and by Coinbase’s user funnel. Analyses cited in external research note that Aerodrome’s stablecoin pools can at times generate roughly twice the fee volume of comparable Curve pools on Ethereum mainnet, though that advantage is dependent on market conditions and Base-specific activity.

Competitive threats are real. Uniswap’s ongoing expansion on Base, the potential roll-out of advanced features like hooks or derivatives, and liquidity migration to lending markets or derivatives protocols can all erode Aerodrome’s dominance. Cross-chain DEX aggregators such as 1inch or CoW Protocol can also reduce its relative edge if they route order flow to competing venues.

Revenue Model and Bribe Markets

Aerodrome’s revenue model is straightforward in structure but complex in incentives. Revenues come from:

- Swap fees collected in the underlying tokens and routed through Gauges.

- External bribes paid by protocols to veAERO holders to attract emissions.

Both revenue streams accrue to veAERO voters, not passive LPs. Liquidity providers earn AERO emissions and indirect benefits from deeper liquidity and volume, but the governance layer is where value concentrates. Bribe markets around Aerodrome are estimated at roughly $150 million annualized, a strong indicator that Base projects view emissions control as strategically important.

The key question is sustainability. Aerodrome’s roadmap includes an emissions “Cruise mode” in which AERO emissions decay by about 1% per epoch starting in Q3 2026. If fee revenue grows fast enough, veAERO yields can transition from inflation-driven to fee-driven without destabilizing liquidity. If not, LPs might rotate to other venues as real yields compress, especially if bribe intensity falls during market downturns.

5. Risk Assessment

Security and Smart Contract Risks

Aerodrome’s codebase inherited a mature design from Velodrome and has been audited by multiple firms, including PeckShield and Quantstamp, with no outstanding critical issues reported at launch. The use of TWAP-based internal pricing for routing adds a layer of protection against short-lived manipulation and flash-loan attacks on individual pools.

Nonetheless, the protocol’s complexity—particularly around Minter–Voter–Gauge interactions and reward distribution contracts—means new features and upgrades must be carefully vetted. The team operates a bug bounty program reportedly funded to around $500,000, which is a positive sign but not a guarantee. To date, there have been no publicly disclosed major exploits, but ongoing monitoring remains essential given the value at stake.

Centralization and Governance Concentration

Two layers of centralization risk stand out.

- Base sequencer centralization: Like other OP Stack L2s, Base currently relies on a centralized sequencer. Any downtime, censorship, or regulatory pressure on Coinbase could directly impact Aerodrome’s liveness and UX.

- veAERO concentration: The top 10 veAERO holders reportedly control around 45% of voting power. Many of these are team-associated wallets and Base-native protocols, which align incentives with ecosystem health but also create a de facto plutocracy in emissions control.

In practice, weekly gauge votes and open bribe markets introduce dynamism and some competitive check on entrenched players. However, new projects without access to large veAERO positions or deep bribe budgets may find it difficult to compete for emissions on equal footing.

Economic and Emissions Risks

Aerodrome’s most significant risk vector is economic rather than purely technical. Its model presumes that:

- Sufficient AERO will be locked as veAERO (currently around 28% of supply) to sustain healthy emission targeting.

- Bribe markets will remain active enough to compensate veAERO holders even as emissions decay.

- Fee revenues will continue to rise with Base adoption, offsetting the inevitable decline in inflationary rewards.

If any of these assumptions break—e.g., if veAERO unlocks spike, if Base growth stalls, or if competition successfully siphons off volume—Aerodrome could face a feedback loop of lower yields, falling TVL, and weaker bribe demand. The design amplifies both positive and negative cycles, which is typical for ve(3,3) systems but important to recognize.

Team, Governance, and Regulatory Exposure

The Aerodrome team benefits from prior experience building Velodrome, and the protocol’s long-running operation without major incidents is a positive signal. Governance is formally decentralized via veAERO, but in practice decision-making power still leans toward early insiders and large ecosystem protocols.

Regulatory risk is indirect but non-trivial. Base’s close association with Coinbase means that any material shift in Coinbase’s regulatory posture, or in policy toward centralized sequencers and fiat on-ramps, could affect liquidity and user flows on Base and, by extension, Aerodrome. This is not a protocol-specific risk, but it shapes the environment in which Aerodrome operates.

6. Ecosystem Impact

Value to Base Users and Builders

For everyday users, Aerodrome is the path of least resistance for trading most mid- to long-tail Base assets. Deep liquidity in stablecoins, blue-chip tokens, and Base-native governance tokens translates to tighter spreads and lower slippage, especially after the rollout of Slipstream pools.

For builders, Aerodrome is even more consequential. Rather than constructing fragmented liquidity across multiple venues, projects can bootstrap via a single, well-understood pipeline:

- Launch a pool on Aerodrome.

- Secure or accumulate veAERO (or bribe veAERO holders) to attract emissions.

- Use growing liquidity as collateral and price discovery input for other protocols (lending, derivatives, yield aggregators).

This pattern explains why roughly 10% of veAERO is reportedly held by Base-native protocols and why at least 15 protocol integrations around veAERO locks and emissions have appeared in early 2026 alone.

Synergies and Network Effects

Aerodrome’s influence compounds as more protocols integrate it:

- Lending protocols (e.g., money markets) rely on Aerodrome’s price and liquidity for collateral assets.

- Yield aggregators and DAOs lock veAERO and optimize bribe strategies on behalf of depositors, deepening the governance market.

- Bridging and wrapped-asset protocols (e.g., for SOL or DOGE representations) use Aerodrome as their primary liquidity venue on Base.

These synergies strengthen the argument that Aerodrome is not just a DEX but a liquidity engine. Liquidity fragmentation on Base is comparatively low, and much of that cohesion can be traced back to Aerodrome’s gravitational pull.

Long-Term Sustainability and Innovation Contribution

Long-term, Aerodrome’s sustainability will hinge on whether it can transition from an emissions-heavy growth phase to a fee-driven, protocol revenue–centric model without losing its dominance. The planned Cruise-mode emissions decay and Flashblocks rollout aim to support that transition by improving capital efficiency and UX as inflation steps down.

As an innovation driver, Aerodrome has already contributed a clear template for how a ve(3,3) MetaDEX can act as chain-level liquidity infrastructure. Its open-source Voter and Minter contracts have been forked and adapted by dozens of projects, and its governance market has become a reference point for Base ecosystem design. Whether this model proliferates across other L2s or remains a Base-centric phenomenon will depend on how successfully Aerodrome navigates the next phase of growth and competition.

7. Investment Perspective

Token Economics and Value Accrual

AERO’s tokenomics are designed to channel value primarily to long-term lockers:

- veAERO lockers receive all protocol fees allocated to voters.

- They also capture external bribes paid to influence emissions.

- Emissions are gradually decaying, increasing the relative importance of fee and bribe income over time.

With approximately 28% of the 1.65 billion circulating AERO locked as veAERO, a substantial portion of supply is effectively removed from liquid circulation in exchange for governance and yield. This lockup supports price stability but also heightens governance concentration, as discussed earlier.

Growth Potential

The bullish case for AERO and Aerodrome is closely tied to Base’s broader trajectory. If Base TVL grows toward the $10 billion range by mid-2026 and Aerodrome maintains even a 50–60% share of that liquidity, the protocol stands to see higher fee revenue, deeper bribe markets, and a more valuable governance layer.

Factors supporting this view include:

- Coinbase’s user funnel (100M+ verified users) feeding into Base.

- Ongoing adoption of Slipstream pools and Flashblocks, reducing slippage and latency.

- Expanding institutional interest in Base and its ecosystem fund connecting capital to builders.

Risk/Reward Profile

Aerodrome and AERO represent a high-beta exposure to Base’s DeFi stack. On the upside, veAERO holders can capture a growing share of Base’s DEX fee and bribe markets if the ecosystem continues to expand and Aerodrome sustains its dominance. On the downside, the protocol is exposed to:

- Emissions and bribe cycles that could compress real yields in bear markets.

- Competitive threats from Uniswap, other DEXs, or novel designs that erode its moat.

- Concentration and governance risks that could discourage some institutional participants.

- Macro-level risk related to Base’s sequencer centralization and Coinbase’s regulatory environment.

For liquidity providers and governance participants, the appeal lies in Aerodrome’s current centrality on Base and the prospect of fee-driven, more sustainable yields over time. The trade-off is meaningful exposure to protocol, ecosystem, and regulatory risk factors that extend beyond typical DEX considerations.

8. Verdict

When Aerodrome launched in August 2023, it could reasonably be viewed as a strategic Velodrome deployment on a promising new L2. By early 2026, the story is different. On-chain metrics, integration patterns, and governance dynamics collectively show that Aerodrome has become Base’s de facto liquidity engine — the primary venue where capital is coordinated, token launches are bootstrapped, and emissions battles are fought.

Technically, Aerodrome combines mature AMM designs with a powerful governance market. Economically, it channels value to long-term veAERO lockers through fees and bribes while offering LPs competitive yields through emissions and concentrated liquidity. Strategically, it is deeply interwoven with Base’s growth story and Coinbase’s broader L2 ambitions.

The trade-offs are clear: governance and sequencer centralization, reliance on emission- and bribe-driven incentives, and exposure to external regulatory and competitive forces. Yet, for Base users and builders, Aerodrome currently sits at the center of the map. Any serious analysis of Base DeFi must start with—and repeatedly return to—how Aerodrome became its liquidity engine, and how resilient that position will prove as the ecosystem matures.

Sources

- Metalamp: “Aerodrome Protocol: How a MetaDEX on Base Blends Uniswap, Curve and Convex”

- PANews: Aerodrome and Base DeFi ecosystem overview

- Binance Square: Aerodrome protocol and mechanism explainer

- Nansen: “What is Aerodrome Finance?” Base ecosystem analysis

- MEXC Research: Aerodrome (AERO) token and ve(3,3) model breakdown

- Exponential.fi: Aerodrome protocol risk and design profile

- Bitget Academy: “What is Aerodrome Finance (AERO)?”

- Aerodrome Finance documentation and app interface (aerodrome.finance)

- DWF Labs research: “Has Aerodrome Finance Become the Leading DeFi Protocol on Base?”